Why Pay as You Go?

Why is pay as you go workers’ comp insurance the right choice for so many businesses these days?

Why is pay as you go workers’ comp insurance the right choice for so many businesses these days?

What is Pay as you Go?

In this video clip, CEO John Will Tenney was interviewed by a local real estate office and answers a few questions about Pay as you Go Payroll and Taxes, as well as Pay as you Go Workers’ Comp. Both of these business options can help reduce costly audits and large bills at the end of a fiscal quarter, or the fiscal year.

A big thank you to Rick Aguirre of Remax Realty of Avalon Park for his help with the video.

Pay as you Go for Workers’ Comp

A “standard” workers’ comp policy comes with some “baggage” that many business owners would like to avoid. Not only are there extra fees for a “standard” policy and a possibly expensive audit every year, there are also some added risks. Why else are so many employers now looking at alternative methods? In today’s economy and business environment it pays to be flexible and innovative.

You may be asking what kind of baggage there is. Have you ever asked these questions?

- Who wants to pay a large premium deposit?

- What is this “expense constant” thing they charge?

- Why is it an estimate?

- Why is there an annual audit that usually ends up costing the business owner more money?

- Why is the timing on the big payment always so bad?

- Why are they telling me I am “mis-coded”?

Does any of this sound familiar in your business? How about these?

- Have you ever wondered why they can’t just take the comp premium at the same time you do payroll?

- Did you even know there are “Pay as you Go” workers’ comp insurance programs available?

- Is the only reason you are NOT doing pay as you go because you think it gives up control of your money?

- What is Pay as you go workers’ comp?”

All good questions. Here are some basic answers. (Please contact us to get more answers.)

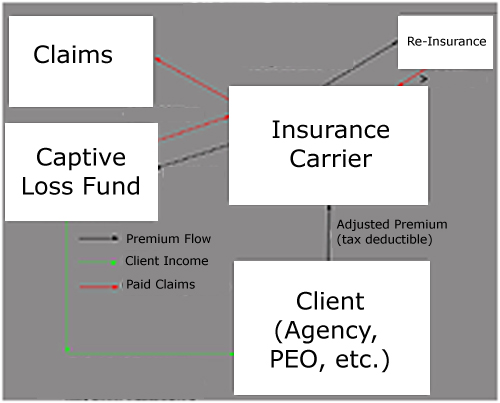

Workers’ Comp premium is figured as a percentage of payroll for each employee in each “class code.” A “class code” is based upon the job description of the employee. For example, clerical employees and roofers have a different class code and of course a completely different rate of premium. “Mis-coding” is when the people are actually working at, or have different duties than those described in the class code.

PEO Pros functions both as a licensed insurance agency and employer consultants to assist employers in this area. Usually this involves placing the employer with a payroll service, or even a PEO. In many cases the payroll service is optional. Yes, you can still enjoy the transferred liability of a PEO without giving up your payroll.

The advantages to pay as you go services are many but here a few headaches that go away:

- Workers’ Comp annual audit is no longer needed

- Tax forms will be filed by the payroll service

- Large premium deposits go away

- Fewer problems predicting cost of employees

- Easier to add employees without incurring insurance increases

- Since reporting is more frequent (each payroll) changes in job description will likely result in less “mis-coding”

If any of this addresses a problem with your business or company, you may want to give us a call at 800.788.8343 or use the form below to contact us with your inquiry: