Hiring and Firing? What’s the Right Way?

Can making a mistake in hiring or firing an employee cost you money? Your business? Your personal possessions?

Can making a mistake in hiring or firing an employee cost you money? Your business? Your personal possessions?

What do you think in this litigious society?

You may be expecting an insurance agency to recommend getting Employment Practices Liability Insurance (EPLI) and it’s not a bad idea, but how about avoiding the need for it as much as possible in the first place?

Is it possible to know the right way to do everything with employees? Possible, but easy? No. It would certainly require staying on top of all the latest laws, practices and codes. Sounds like a lot of research to us.

Wouldn’t it be easier to have it be Somebody Else’s Problem?

Entering in to PEO relationship may be an easier (and safer) solution. After all, it is their job to handle all the employee issues related to employment. In most cases their EPLI policy offers you, the employer, some coverage as well.

Here is a brief story from one of our clients:

“A few years ago we had an employee who was not performing satisfactorily. We didn’t know what to do. She was very well liked and a personal friend of ours. We tried to talk to her but she told us what ‘we wanted to hear’ and still failed to do her job satisfactorily.

We decided to call our PEO. After a very relaxing call we asked ourselves, ‘Why didn’t we do this before?’ After all, they are professionals aren’t they?

They handled it very well. They called our employee and asked if she knew what her job duties were. She listed them fairly accurately. They asked her if she could complete those tasks in the next two weeks. She said yes. They scheduled a phone meeting at the end of the two weeks. They went down the list with her and asked her if she had completed the tasks. Not surprisingly, she hadn’t completed more than a couple. They asked her ‘What should we do?’ She said ‘I guess I shouldn’t be at this job’ and they offered her a chance to resign rather than be terminated for cause. She took it.

When she handed in her resignation to us she told us that the PEO did a great job and she apologized for wasting our time. We took her out for a farewell lunch and she told us she already had a new position lined up. In fact, she entered a new career that suits her better and we are still friends. FOrgive us for stealing someone else’s tag line but:

‘That was easy’

Thanks to PEO Pros for putting us with such a Professional Employer Organization.”

If you want to have less stress and a more comfortable relationship with your employees, consider asking us to match you with the right PEO.

At PEO Pros, we are your professional PEO matchmakers. Use the contact form below for more information.

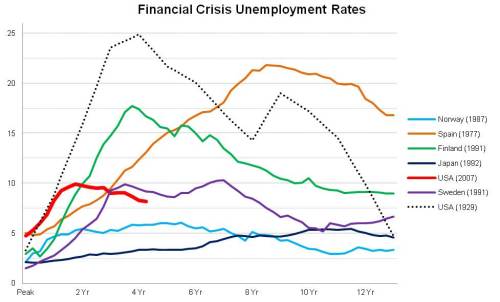

As if Obamacare isn’t bad enough, now small employers have to worry about the complex issue of rising unemployment insurance and tax rates. Formerly a rather simple calculation, things have happened in several states that make things complicated.

As if Obamacare isn’t bad enough, now small employers have to worry about the complex issue of rising unemployment insurance and tax rates. Formerly a rather simple calculation, things have happened in several states that make things complicated. “What effect will Obamacare have on employers?”

“What effect will Obamacare have on employers?”